NAIOP, the Commercial Real Estate Development Association, just published the results of its excellent biannual investor survey. The NAIOP CRE Sentiment Index summarizes the predictions of approximately 5,000 commercial real estate investors, developers and operators about general conditions in the commercial real estate industry in 2018. .![]()

Admiral’s Jon Gordon weighs in on what current investor sentiment means for commercial real estate investors in Westchester County in the next year.

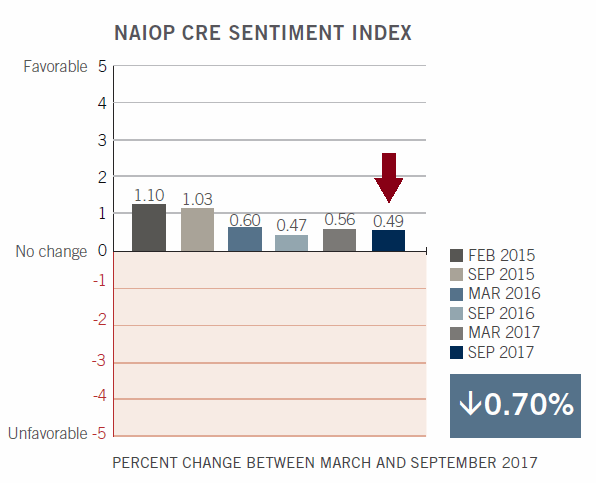

Not a Lot of Change Expected

Overall, forecasts for 2018 are on the slightly positive side of neutral (+0.49 out of a range of -5.00 to +5.00), with limited changes expected over the next 12 months. This represents a small decline from six months prior.

.

.

According to the survey:

- Employment is expected to be strong, with many respondents planning to hire more people in 2018 than in 2017.

- Growth in occupancy rates is expected to slow as the cycle matures.

- Positive rent growth is predicted. Face rents are likely to increase more than effective rents due to potential increases in operating costs and/or concessions. Effective rents are expected to improve more for industrial than for office or retail.

- Significant increases in construction materials and labor costs will dampen the market. Insurance costs also likely to rise. (It is important to note that responses to the survey were completed between 9/6/17 – 9/18/17. As such, the survey took into account rebuilding efforts relating to Hurricanes Harvey and Irma, but not the potential effects of subsequent events, such as Mexico’s 9/19 earthquake and Hurricane Maria in Puerto Rico.)

- While not to the point of plentiful, respondents expect adequate availability of debt and equity in 2018. Curiously, there was no discussion of the impact of likely interest rate increases. As of September, the Fed projected a median federal funds rate of 1.4% in 2017, rising to 2.1% in 2018 and to 2.7% in 2019. Any such increases would have an immediate impact on the prime rate, and would likely affect financing costs over the longer-term.

- First-year capitalization rates are expected to increase slightly, reflecting respondents’ anticipation of an increase in overall project risk.

Quotes from Respondents

We find direct quotes from survey respondents particularly helpful in understanding what is driving their expectations, and fears. Recurring concerns include geopolitical uncertainty, ‘black swan’ events, and divergence in economic growth:

.

“I am nervous about geopolitical issues…[and] the widening wealth gap in the USA.”

“The large and coastal regions and markets will do fine; secondary/tertiary markets are starting to suffer from poor local economies as all things consolidate to major population centers.”

“Things remain competitive on the acquisition front, but I think the bulk of the cap rate compression is done. But there is still too much capital chasing too few deals.”

“Fundamentals are still solid and development hasn’t gotten out of line, but the cycle feels mature and pricing is past peak levels in many markets.”

“Demand remains strong in the markets we’re looking to acquire in, so as long as investors stay disciplined, I don’t think the market will change a whole lot over the next 12 months, unless there is a black swan event on the horizon.”

Admiral’s Outlook for Westchester Real Estate Investors

Cap rate compression and rising operating expenses have encouraged many investors to look outside of Manhattan and into nearby secondary markets such as Westchester. Due to its relative safety and stability, Westchester has benefited from this change with an expanding pool of buyers. However, lack of available product has limited sales volume.

Consequently, discretionary sellers will drive the Westchester market in the next 12-18 months. As interest rates continue their slow climb upward, capitalization rates will expand in tandem, for all but the best assets. Prime assets in the most vibrant Westchester markets will have below market capitalization rates, as all-cash buyers who are sitting on significant non-deployed cash bid aggressively on those buildings. Whether multifamily, retail or industrial, well-located properties with reliable cash flow sell fairly quickly if priced correctly.

As the cost of capital increases and cap rates expand, discretionary sellers – who are not forced to sell – will have to decide if they are willing to adjust their prices from recent historic highs. A low number of discretionary sellers will limit available properties, causing more competition among buyers and thereby bolstering property values. A high number of discretionary sellers, on the other hand, will accelerate cap rate expansion, especially as capital costs rise.

Of course a seesaw is seldom in perfect balance. Comments from NAIOP’s survey respondents allude to concerns that a sudden catastrophic event, or a slow deterioration in confidence or the economy, can change both buyers’ and discretionary sellers’ willingness to enter the market, and their price sensitivity. Barring unforeseen events, however, the Westchester market should remain steady for the next 12 months, slanting toward sellers.

.

.For more information, please contact Jonathan Gordon, President/CEO or call 914.779.8200 x115

AVAILABLE PROPERTIES

.

Admiral Real Estate Services Corp. is a commercial real estate brokerage firm offering investment sales, agency leasing and tenant representation services. Based in Westchester, the company currently lists and/or manages over 100 retail, office and development properties in the New York metropolitan area.

_________________________________________

.Tags: real estate investor, naiop, CRE sentiment index, commercial real estate, real estate outlook, real estate market